By Mark Roe (Harvard Law School) and Vasile Rotaru (Harvard Law School; University of Oxford)

Coercive, non-pro rata debt restructurings—now widely labeled “liability management exercises” (LMEs), just like their pro rata siblings—have become a central tool for distressed borrowers. Proponents of the non-pro rata restructuring often argue that it gives the company time to turn around and take off, reduce financial distress, and typically avoid bankruptcy.

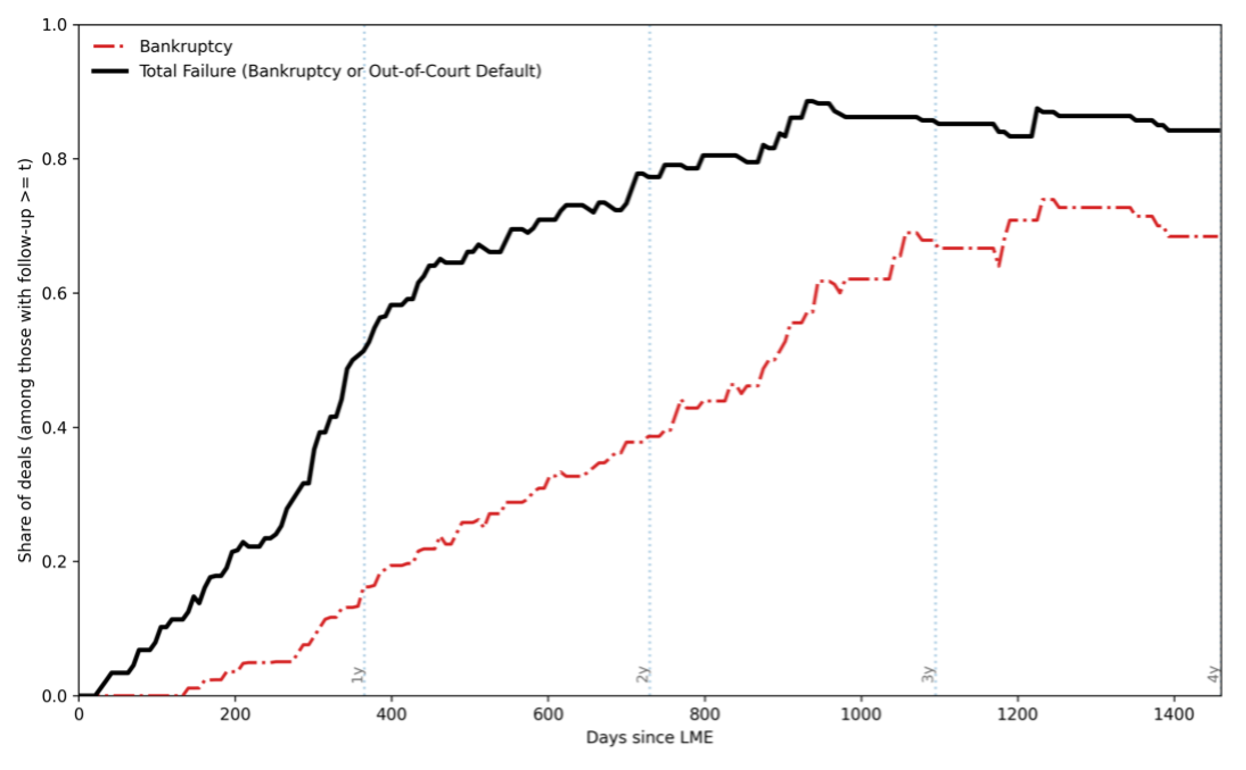

Our new paper argues that this expectation is overstated: on average, LMEs buy a shorter, more fragile runway than proponents suggest; most coercive LMEs in our sample ultimately default again or file for bankruptcy anyway.

An LME, broadly, is simply an out-of-court debt renegotiation—yesterday’s “workouts.” In recent years, the neutral LME label has displaced the blunter “creditor-on-creditor violence” descriptor for transactions in which debtors pit creditors against each other and align with winning coalitions to shift value from others (“dropdowns”) or elevate participating creditors’ priority (“uptiers”) in exchange for runway extension.

Some creditors lose, some win. Some lose in this deal but win in the next. But—proponents argue—these are typically sophisticated, diversified investors, and coercion is needed to break coordination and free-rider problems that would otherwise push firms into bankruptcy. In restructuring circles, well-known “success stories” are celebrated: runway extended, bankruptcy avoided, operations revived.

Some coercive LMEs do benefit firms and stakeholders. But does the celebratory story reflect typical outcomes?

First off, we show that the structural imperatives of a coercive LME deal militate toward a more complex capital structure, with limited deleveraging and limited debt-to-equity conversions. To make the uptier work, the majority creditors typically need higher priority debt, not lower priority equity. If these forces are strong, they can impede balance sheet stabilization. And shifting value from excluded creditors to the dealmakers can benefit owners and favored creditors even if the firm is no better off—and even in theory if it’s made worse off.

Hence, the abstract incentives could produce good operational outcomes and more stable balance sheets. Or they could just shift value with limited benefits to the firm.

We examine what’s happening on-the-ground. Ours is the first study to test average firm-level effects, based on a hand-collected dataset of 89 coercive, non-pro rata LMEs.

The results are sobering.

Within one year of an LME, fewer than half avoided bankruptcy or re-default; within two years, only 22% avoided both. Among firms with at least two years of post-LME history, 56% had already filed for bankruptcy. These figures sit uneasily with the bankruptcy-avoidance narrative.

For comparison, the LME relapse rate far exceeds our estimated relapse rates for prepackaged bankruptcies—which are often achieved with similar levels of creditor support.

The average firm-level benefits are also unclear. Credit ratings remain largely flat for two years after an LME, reflecting persistently high default risk as assessed by rating agencies.

Debtors sometimes secure new money, but aggregate leverage doesn’t decline—indeed, deleveraging is well below typical prepackaged-bankruptcy outcomes. Instead of stabilizing balance sheets through debt–equity swaps, LMEs often elevate favored creditors, leaving thin equity cushions with distorted incentives. More cumbersome capital structures prolong debt overhang and can make a full turnaround and takeoff harder.

Finally, LME debtors that go bankrupt spend, on average, two-to-three times longer in bankruptcy than non-LME prepacks or PE-backed debtors.

Some qualifications: we evaluate non-pro-rata LMEs, not plain-vanilla, pro-rata restructurings, whose incentive structures give fewer reasons to expect inefficient outcomes. Moreover, we rely on leading industry information sources, but some coercive LMEs may go unreported. Lastly, most reported LMEs involve private firms that do not disclose operating data (EBITDA, sales, and so on); comparing these measures pre-LME and post-LME would be more probative of their success or failure. That said, the best evidence available now is in our paper, and it undermines the coercive-LME celebratory story.

We then analyze the implications: Why have coercive, non-pro rata LMEs spread over the past decade if they typically do not solve the firm’s operational and financial problems? Why have markets not yet closed the contractual loopholes that enable them, and are there signs that markets might self-correct in the future? What do our findings say about the American financial system today? And what do they imply for LME litigation, for contract-interpretation and for fiduciary-duty obligations?

Click here to read the full article. A Financial Times profile of the paper is available here.